Every year, a significant number of high-net-worth individuals make the same expensive mistake: they buy a luxury property in Marbella or Andalusia either in their own name when they should have used a company — or through a company when personal ownership would have served them far better. The tax consequences can run into hundreds of thousands of euros.

This article gives you the framework we use at Utrust when advising clients on property deal structures. It is not a one-size-fits-all answer — because there is no such thing. The right structure depends entirely on your goals: rental income, personal use, inheritance planning, future exit, or a combination of all four

This article gives you the framework we use at Utrust when advising clients on property deal structures. It is not a one-size-fits-all answer — because there is no such thing. The right structure depends entirely on your goals: rental income, personal use, inheritance planning, future exit, or a combination of all four

The market context: Marbella's Golden Mile now commands €6,422/m² on average, with ultra-prime beachfront stock at Puente Romano reaching €24,020/m² in 2025. At these price points, structuring the acquisition correctly is not optional — it is a core part of the investment.

The Baseline: Taxes Are the Same at Acquisition

Let us address the most common misconception immediately. Whether you buy a resale property in Andalusia as a private individual or through a Spanish Sociedad Limitada (SL), the acquisition taxes are identical:

*Regardless of whether the buyer is an individual or a company, if the seller is a company, the transaction will generally be subject to VAT, except in certain specific cases provided for by law.

Andalusia unified its ITP structure introducing a clean 7% flat rate for all second-hand residential property. There is no progressive surcharge for high-value properties — unlike Valencia (where properties above €1M attract 11%) or Catalonia. This fiscal simplicity is one reason high-net-worth buyers continue to favour the Costa del Sol.

The 2% resale ITP rate does exist in Andalusia, but only when an SL acquires a property specifically for resale within two years. This is a legitimate planning tool for developers and flippers, but it requires documented business intent and comes with conditions.

When Personal Ownership is the Right Answer

For most luxury buyers on the Costa del Sol, purchasing in your own name is not only simpler — it is genuinely more tax-efficient in a number of scenarios.

Scenario 1: Primary or secondary residence for personal use

If the property will be used personally — as a full-time residence or holiday home with minimal or no rental income — the SL structure creates costs and obligations without proportional benefit. An SL that owns a property you use personally creates a taxable benefit-in-kind: the Spanish Tax Agency (AEAT) requires that you pay market rent to your own company. Fail to do this correctly and the company faces an imputed rental income liability at 25% corporate tax.

Scenario 2: Primary residence and future sale with reinvestment

If you intend to sell and buy a new main residence, Spanish law grants individual owners a capital gains reinvestment exemption. Companies cannot claim this. A company pays 25% corporate tax on the entire gain. An individual can defer or eliminate that tax entirely by reinvesting in a new habitual residence.

In addition, for non-resident individuals selling a property in Spain, the capital gains tax depends on the country of residence. For residents of the EU, the tax rate is 19%. For residents outside the EU, the tax rate is 24%.

Scenario 3: Andalusia inheritance, near-zero tax for close family

The regional government applies a 99% reduction on inheritance for direct family (spouses, children, parents), and the first €1 million per heir is also exempt. In practice, inheritance tax for a husband leaving a €3M Marbella villa to his wife and two children is effectively zero. Transferring shares of an SL to heirs does not benefit from these personal allowances in the same way.

When the SL Structure Unlocks Real Value:

The calculation changes significantly for buyers with a commercial property strategy, a large portfolio, or specific estate planning objectives.

1. Rental income: the most compelling case

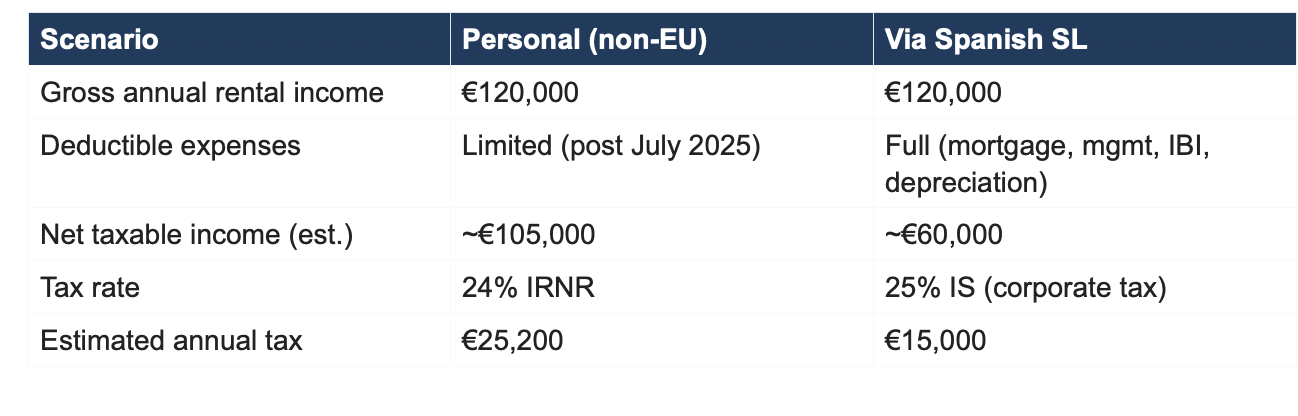

This is where the SL delivers its clearest advantage. Consider a non-EU resident (US, UK, Middle Eastern buyer) renting out a Marbella villa. Under personal ownership, they face a flat 24% IRNR (Non-Resident Income Tax) with zero expense deductions.

Under an SL, the company pays 25% corporate tax — but on net profit after full deduction of mortgage interest, management fees, insurance, IBI, maintenance, and crucially, 3% annual depreciation of the building value. On a property acquired at €3M, that depreciation alone saves approximately €22,500 per year in taxable base. Over a ten-year holding period, the SL typically outperforms personal ownership on pure tax efficiency — often dramatically so.

Under an SL, the company pays 25% corporate tax — but on net profit after full deduction of mortgage interest, management fees, insurance, IBI, maintenance, and crucially, 3% annual depreciation of the building value. On a property acquired at €3M, that depreciation alone saves approximately €22,500 per year in taxable base. Over a ten-year holding period, the SL typically outperforms personal ownership on pure tax efficiency — often dramatically so.

Note: figures are illustrative and depend on actual expenses. Always model your specific numbers with a qualified tax advisor.

2. Portfolio strategy: multiple properties

For buyers acquiring three or more properties, the SL becomes the operational backbone of the portfolio. It centralises administration, allows cross-property cost allocation, and enables intra-group financing structures. It also provides the foundation if you later wish to migrate to a SOCIMI (Spanish REIT) structure — relevant for portfolios exceeding €5M with at least eight properties.

3. Exit strategy: selling shares

In some corporate structures, it may be possible to transfer the shares of a company that owns real estate instead of selling the property itself. Share transfers are generally subject to a lower transfer tax (around 1%). However, Spanish law includes anti-avoidance rules that apply when the company mainly holds real estate and the buyer acquires control. In those cases, the transaction is taxed as if the property itself were sold, and the buyer must pay the standard real estate transfer tax (around 7% in Andalucía). Therefore, the tax advantage of selling shares instead of the property depends heavily on the structure of the company and the nature of its activity.

4. Wealth tax optimisation

Andalusia and Madrid both apply 100% regional wealth tax relief. However, Spain's national Solidarity Tax on net assets above €3M remains in force. For buyers with a Spanish real estate portfolio above this threshold, holding assets through a correctly structured SL — with genuine economic activity — can reduce or eliminate the Solidarity Tax base.

At utrust, we advise high-net-worth buyers and family offices on deal structuring for Spanish real estate from initial acquisition to exit. If you are evaluating a property acquisition above €1M in Marbella or Andalusia, speak with us before signing any private contract.